INVESTMENT AND ESTABLISHMENT OF EXPORT PROCESSING ENTERPRISES IN VIETNAM

- OVERVIEW OF EXPORT PROCESSING ENTERPRISES

- Definitions

Export processing enterprises:

EPE is an enterprise specializing in producing export goods, performing services for the production of export goods and export activities are established and operated in accordance with the Government's regulations on export processing enterprises.

Pursuant to Article 2 of Decree 35/2022/ND-CP stipulates that "Export processing enterprises are enterprises carrying out export processing activities in export processing zones, industrial parks and economic zones".

Export Processing Zone:

Pursuant to Article 1 of the Vietnam Export Processing Zone Regulation (issued together with Decree No. 332- HDBT dated October 18, 1991 of the Council of Ministers), it stipulates:

The export processing zone is an industrial park specializing in the production of export goods and carrying out export and export production services established and operating under this regulation.

The exchange of goods between export processing enterprises and enterprises in the Vietnamese market is considered import and export relations and must comply with the provisions of the law on import and export.

EPE are exempt from export and import taxes on goods exported from export processing zones to foreign countries or imported into export processing zones, and are given duty incentives in the case of special investment incentives under Vietnamese law.

- Characteristics of EPE

First, the production of goods for export is in the majority

This is an industrial park dedicated to enterprises specializing in the production of goods exported abroad. Including enterprises providing services related to import and export activities.

Second, the geographical location is isolated from the outside

Because they are located in export processing zones, industrial parks, and economic zones, export processing enterprises are separated from the external territory by a system of fences, entrance gates, and doors for customs officials and relevant authorities to inspect, supervise, and control .

Third, enjoy special offers

EPE is exempt from export tax, import tax on goods from export processing zones exported abroad or from abroad imported into export processing zones, and receives tax incentives in the case of incentives, especially investment incentives, in accordance with the provisions of Vietnamese law

Finally, EPE must meet special conditions

For EPE, individuals, organizations and investors are required to meet certain conditions before implementing business investment projects. In addition, EPE also needs to fully comply with the requirements of customs authorities related to non-tariff zones and regulations on import and export taxes.

II. NOTES WHEN INVESTING AND ESTABLISHING EXPORT PROCESSING ENTERPRISES IN VIETNAM

Export processing enterprises are not distinguishable from other types of businesses (such as limited liability companies, joint stock companies, partnerships, and sole proprietorships; groups of companies). EPE is merely an enterprise with defined conditions and specific production and business activities. Therefore, the regulations on the establishment of export processing enterprises are similar to those for other enterprises. However, investors should note that the establishment conditions apply separately to the establishment of export processing enterprises specified in Clause 2 of Article 26 of Decree 35/2022/ND-CP. In particular:

- Geographical separation conditions

Export processing zones, export processing enterprises, and industrial subdivisions for export processing enterprises are separated from external territories by a system of fences, gates, and doors, according to the regulations applicable to non-tariff zones specified in the law on export and import taxes.

Specifically, Clause 17 of Article 2 of Decree 35/2022/ND-CP stipulates: "Free trade zone in an economic zone" refers to a free zone specified in the master plan for construction of an economic zone. When constructing economic zones or border gate economic zones, the geographical boundaries of the non-tariff zone are defined in the general plan, which is approved by competent agencies in accordance with the provisions of law.

- Ensuring conditions for customs inspection and supervision

Export processing enterprises must ensure conditions for inspection, supervision, and control by customs authorities and relevant authorities in accordance with regulations applicable to non-tariff zones according to the law on export tax and import tax.

According to Decree 18/2021/ND-CP on customs inspection and supervision, conditions for export processing enterprises that are in non-tariff zones must meet all conditions: must have a hard fence separating it from the outside area; there are gates/doors, ensuring the delivery of goods into and out of export processing enterprises only through those gates or doors; must have a CCTV system for positions at gates/doors, entrances, and storage locations at all times of the day (including holidays); Camera image data is connected online with the customs authority managing the enterprise and stored at the export processing enterprise

III. CURRENT STATUS OF EXPORT PROCESSING ZONES AND EXPORT PROCESSING ENTERPRISES IN VIETNAM IN VIETNAM

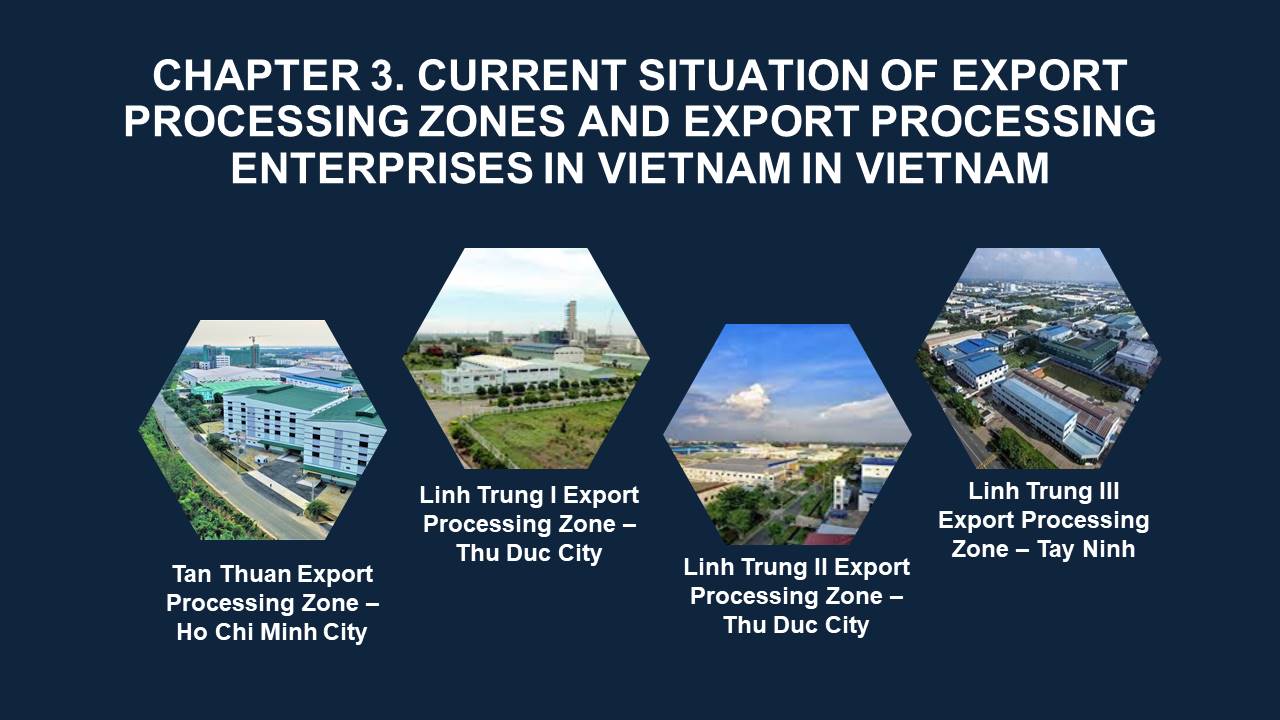

According to data provided by VnEconomy – e-magazine of the Vietnam Economic Science Association, by the beginning of 2022, Vietnam is estimated to have 395 export processing zones and industrial parks in 61 provinces and cities with a planned area of up to 123,000 hectares. In particular, the 4 largest export processing zones, bringing the most significant efficiency include: Tu Thuan Processing Zone, Linh Trung I, Linh Trung II and Linh Trung III.

Tan Thuan Export Processing Zone – Ho Chi Minh City

Tan Thuan Export Processing Zone was established in 1992 with a total investment of 1,690 billion USD. Up to now, there have been 199 investors from 20 different countries and territories around the world participating in investment and production. software and high technology, household appliances, electronics, mechanics, textiles, pharmaceuticals, cosmetics, sports equipment, plastics, packaging ... Some typical enterprises in Tan Thuan export processing zone can be mentioned as:

- Sanyo Semiconductor Co.ltd

- Vina Alliance Co., Ltd

- Toyo Precision Co., Ltd.

- Aricent Vietnam Co., Ltd

- Wonderful Saigon Garment Co., Ltd

- Nidec Tosok Co., Ltd.

- D&Y Technology Vietnam Co., Ltd.

Established in 1995 with more than 62 hectares area of lands, Linh Trung I export processing zone has attracted many businesses with effective production and business activities such as:

- 99 Vina Co., Ltd

- Fenix knitwear Co., Ltd

- Fuji Impulse VN Co., Ltd

- Hugo Knit Co., Ltd

- JYE Shing Industry Co., Ltd

- Kachiboshi VN Co., Ltd

Linh Trung II Export Processing Zone - Thu Duc city

Linh Trung II Export Processing Zone is located in Binh Chieu Ward, Thu Duc District City on an area of 61.7 hectares. After nearly 22 years of operation, the Linh Trung II export processing zone has brought about certain contributions to the economy of Ho Chi Minh City in particular and the whole country in general, contributing to increasing export turnover as well as the economic growth of the country.

The export processing enterprises in the Linh Trung II operate mainly in the fields of food and foodstuffs, machinery processing, electronics, mold manufacturing, plating, etc. and come from many countries around the world such as Korea. China, Japan, Taiwan, etc. Some typical enterprises can be mentioned as:

- Iwasaki Co., Ltd

- SAP VN Co., Ltd

- Ricco Việt Nam Co., Ltd

- Sadev Decolletage VN Co., Ltd

- Meinan Co., Ltd

- Supper Art VN Co., Ltd

Linh Trung III Export Processing Zone - Tay Ninh

Linh Trung III was established later than the previous three export processing zones and has a much larger land area, up to 203.8 hectares. This export processing zone is a joint venture project between Vietnam and China, located in Tay Ninh, with production and business activities of enterprises mainly in the following industries: production of consumer goods, garments, mechanical engineering, electronics, chemicals, and tobacco. Some big businesses here can be named:

- Han Viet Rubber Roll Co., Ltd

- Hansae Co., Ltd

- Dou Power Co., Ltd

- Viso Pacific Co., Ltd

- Playloud Co., Ltd

- Kataragi Co., Ltd

IV. DEVELOPMENT POTENTIAL OF EXPORT PROCESSING ENTERPRISES IN VIETNAM

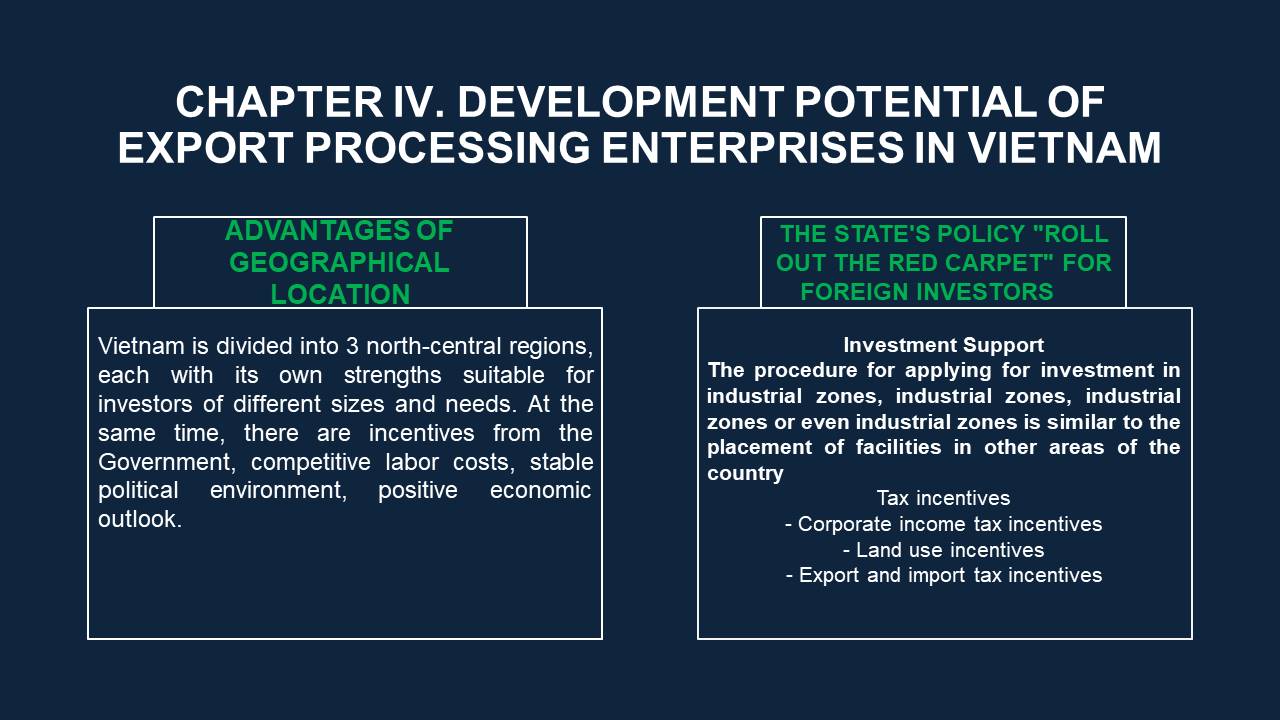

- Geographical advantages

Vietnam is divided into three regions: North, Central, and South; each region has unique strengths that are appropriate for investors of various sizes and needs. At the same time, there are incentives from the government, competitive labor costs, a stable political environment, a positive economic outlook, and free trade agreements that have been signed.

Due to its proximity to the North, the Northern industrial market is a good choice for global manufacturers wishing to expand their factories outside of China. The industrial market in the North shines thanks to the focus on investment in education and synchronous development infrastructure.

With a synchronously developed network of sea, railway, road, and aviation networks, Ho Chi Minh City and neighboring provinces are the most vibrant economic regions in the country and an appropriate destination for manufacturers. new export to Vietnam. Thanks to a large land bank with lower rents than other areas and a dense seaport system, the Central region is an attractive destination for many international industrial manufacturers.

The policy of the state is "rolling out the red carpet" for foreign investors.

- Investment support

The procedure for applying for investment in an IZ, EPZ, EZ or even an IZ is similar to setting up a base in other regions of the country, but the review and licensing process is easier. For example, for investment projects implemented in IZs or IZs, the investment licensing agency considers approving the investment policy and the investor without holding an auction of land use rights, and instead bids to select investors. In addition, investors with investment projects in industrial zones (EPZs, EZs, or IZs) are also supported by competent state agencies in carrying out administrative procedures on investment, enterprises, land, construction, etc., environment, labor, and trade under the "one-stop shop, on-site" mechanism, providing support on labor recruitment and other related issues during project implementation.

The Law on Investment in 2020 has added a type of investment incentives, the most prominent of which is "fast depreciation." This is a form of incentive to help businesses and investors reach the breakeven point faster. In addition, the tax-deductible expenses have been increased.

- Tax incentives

Export-processing enterprises are entitled to a number of tax incentives, as follows:

First, corporate income tax incentives

Pursuant to Clause 4, Article 19 of Circular 78/2014/TT-BTC, export processing enterprises are entitled to the reduced tax rate of 17% from January 1, 2016, when they implement new investment projects in socio-economically difficult areas listed in Appendix II to Decree 118/2014/ND-CP (Article 66 of Decree 118/2014/ND-CP).

At the same time, export processing enterprises are also entitled to a 2-year tax exemption and a 50% reduction of payable tax amounts for the next 4 years for incomes from the implementation of new investment projects specified in Clause 4, Article 19 of Circular No. 78/2014/TT-BTC as above (Article 6 of Circular 151/2014/TT-BTC).

Second, preferential land use fee

Export processing enterprises are exempted from land rent for 7 years (point b, clause 3, Article 19 of Decree 46/2014/ND-CP).

In addition, according to Article 27 of Decree 68/2017/ND-CP, production and business investment projects in industrial clusters are exempt from land rent for 7 years and enjoy other incentives as prescribed by law. When there are multiple incentive levels, the highest incentive rate applies. Article 19 of Decree 46/2014/ND-CP)

Third, preferential import and export tax

Pursuant to Point c, Clause 4, Article 2 of the 2016 Law on Import and Export Taxes, goods exported from non-tariff zones to foreign countries; goods imported from abroad into non-tariff zones and used only in non-tariff zones; and goods moved from one non-tariff area to another are not subject to tax. Export processing enterprises are located in a non-tariff zone, so they will not be subject to import and export tax in the above cases, also known as the application of 0% tax.

V. Conclusion

Vietnam has all the factors to become a bright investment destination. From the natural resources and social conditions, to the political institutions, the country's development direction is towards the goal of developing Vietnam's industry. Export processing enterprises in particular and industrial production enterprises in general are important factors in implementing the national policy of industrialization and modernization that the government is prioritizing. The above incentives are proof of that, which means that foreign businesses will always receive the best support from state agencies.

For export processing enterprises alone, there will be large investors who want to produce goods with the highest quality for export purposes. Accompanying the benefits is the responsibility to meet the strict regulations of Vietnamese law. With experience in investment law consulting for businesses from many countries, DHT confidently provides consulting services to set up businesses in Vietnam, as well as consulting and answering questions for investors. We are very pleased to accompany investors in the process of creating businesses.