ELECTRONIC-CUSTOMS PROCEDURES ON IMPORT-EXPORT ACTIVITIES OF EXPORT PROCESSING ENTERPRISE UNDER VIETNAMESE LAW

1. Overview of electronic-customs procedures:

1.1. Definition

According to Clause 1 Article 3 of Decree No. 08/2015/ND-CP, electronic-customs procedures refers to customs procedures under which the information used for the customs declaration shall be provided, received and processed, and the exchange of other information between parties involved shall be carried out through the electronic data processing system, as stipulated by the applicable law on customs procedures.

1.2. Subjects of electronic-customs procedures

According to Article 2 of Circular No. 22/2014/TT-BTC, the subjects of electronic-customs procedures include :

- Organizations and individuals that apply electronic-customs procedures to import and export commercial goods: These are the direct beneficiaries of electronic customs procedures. Enterprises can register an account on the system and use its features to carry out customs procedures quickly and conveniently.

- Customs authorities: Customs authorities can use electronic-customs procedures to manage import and export activities, inspect and process customs documents, and obtain related information on goods.

- Other related units: Besides enterprises and customs authorities, other related units such as banks, transportation, and insurance companies can also use electronic-customs procedures to interact with the system and carry out transactions related to import and export.

1.3. Advantages and disadvantages of electronic-customs procedures

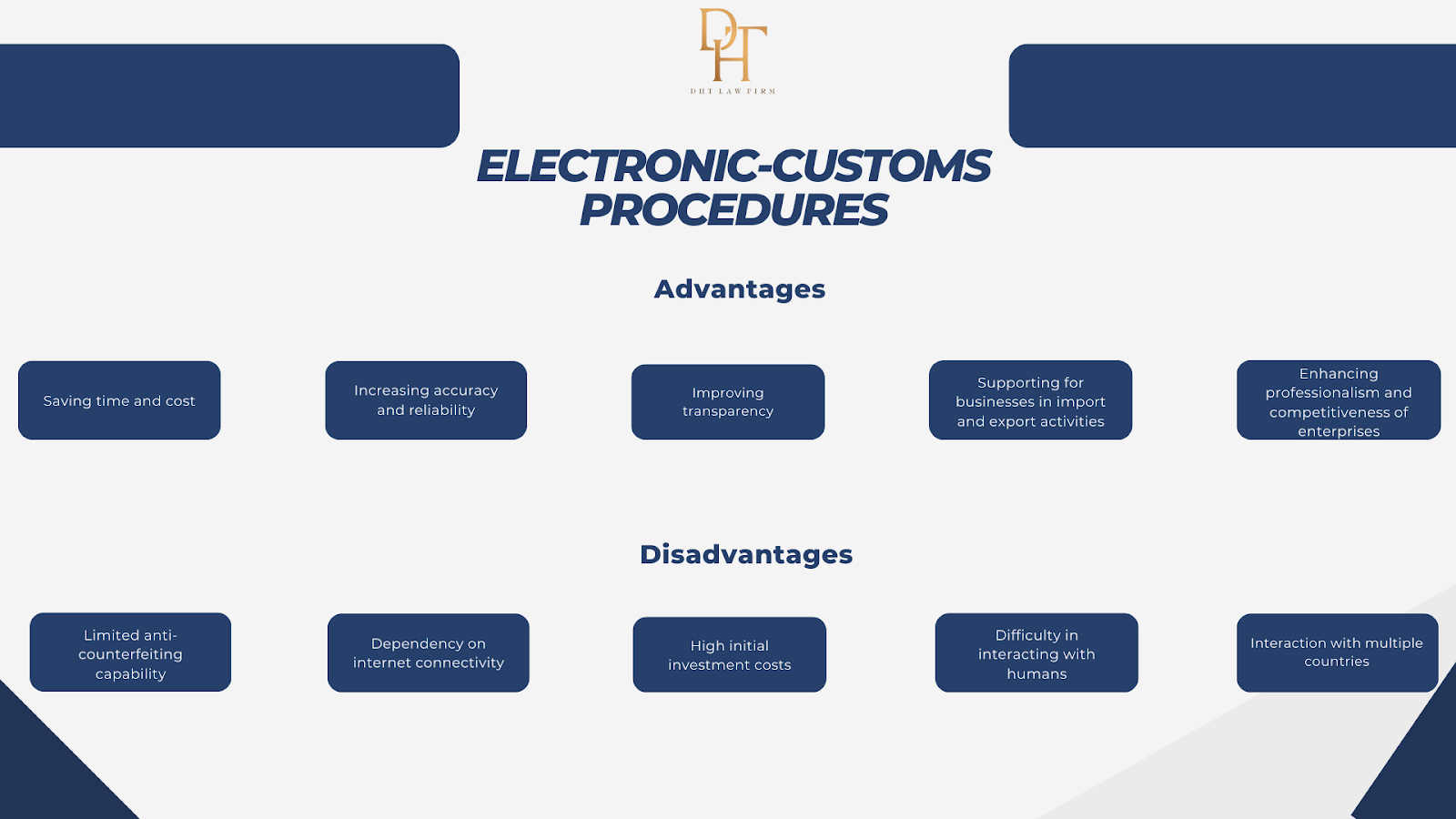

1.3.1. Advantages

- Saving time and cost: Electronic-customs procedures provide convenience for businesses to carry out procedures quickly and conveniently without traveling to customs authorities to submit documents. This helps businesses save time and costs related to transportation and shipping fees.

- Increasing accuracy and reliability: Electronic-customs procedures ensure that information related to goods is updated and managed accurately and quickly, avoiding errors during the process. This also contributes to making the process of controlling and managing goods more efficient and in accordance with procedures.

- Improving transparency: Electronic-customs procedures make tracking and controlling transactions related to goods more transparent, clearer and easier. Enterprises can easily access and retrieve information about their customs procedures.

- Supporting businesses in import and export activities: Electronic-customs procedures enable enterprises to carry out customs procedures conveniently and quickly, thereby creating favorable conditions for transportation and import-export of goods.

- Enhancing professionalism and competitiveness of enterprises: The use of electronic technology in performing customs procedures demonstrates the advancement and professionalism of enterprises, thereby increasing their competitiveness in the international market. Enterprises using electronic-customs procedures also have the opportunity to access potential markets for their expansion.

1.3.2. Disadvantages

- Limited anti-counterfeiting capability: Electronic customs may face difficulties in verifying the validity of documents and information as they are affected by increasingly sophisticated counterfeiting technologies.

- Dependency on internet connectivity: To operate efficiently, electronic-customs require continuous network connectivity. If the network connection is interrupted, the system will not function properly and may lead to incidents.

- High initial investment costs: Implementing electronic-customs requires a large amount of capital investment for the necessary equipment and relevant systems. This can put pressure on budgets and require significant investment from governments.

- Difficulty in interacting with humans: Electronic-customs cannot completely replace human interaction. In some cases, there needs to be interaction between automated systems and humans to ensure that the verification process is carried out accurately.

- Interaction with multiple countries: Electronic customs require countries to participate and interact with each other to ensure that the processes of checking and classifying goods are carried out correctly. This requires cooperation and sharing of information between countries, which may not always be easy.

2. Regulations on electronic-customs procedures for export and import goods of export processing enterprises under Vietnamese law.

2.1. Regulations on registering accounts and using electronic-customs software

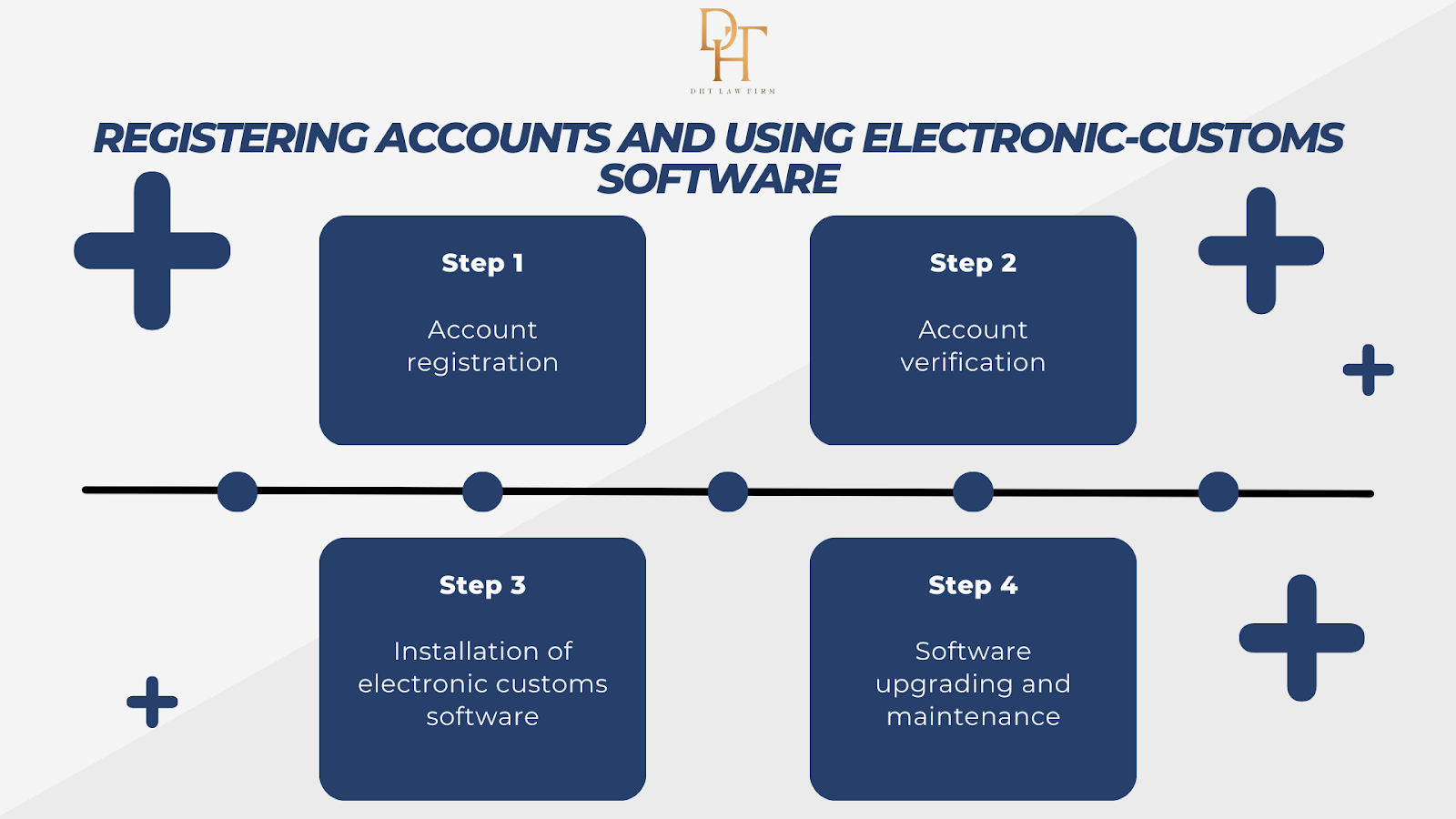

According to the regulations of the Law on Customs 2014 and relevant guidance documents, enterprises need to register an account on the electronic-customs system to use online services related to import and export of goods.

Specifically, the regulations on registering accounts and using electronic-customs software are as follows:

- Step 1: Account registration: Enterprises need to register an account on the electronic-customs system through the link provided on the General Department of Customs' website. The account registration process requires enterprises to provide information about their username, password, and information about the enterprise.

- Step 2: Account verification: After registering an account, enterprises need to verify their account by going to customs authorities to carry out the account verification process.

- Step 3: Installation of electronic customs software: After having an account and being verified, enterprises can install electronic-customs software to use the system's features.

- Step 4: Software upgrading and maintenance: Enterprises using electronic-customs software need to regularly upgrade and maintain the software to ensure system stability and security.

In addition, enterprises using electronic-customs procedures must comply with regulations associated with information security and electronic authentication, and ensure that information related to import and export of goods complies with legal requirements.

2.2. Regulations on electronic-customs declaration, tax and fee payment, inspection and processing.

2.2.1. Electronic-customs declaration.

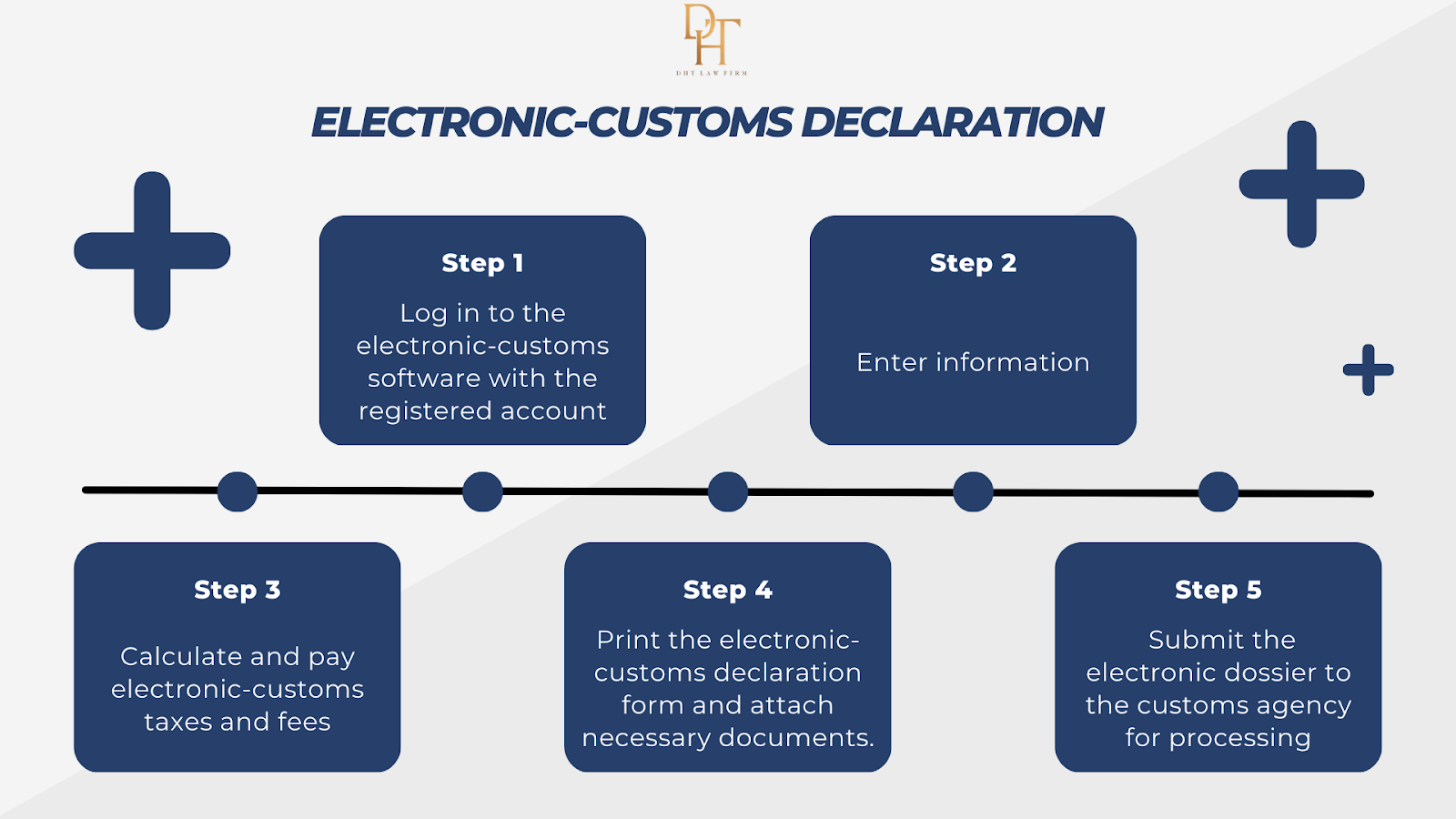

According to the regulations of the Customs Law 2014 and Circular No. 39/2018/TT-BTC, enterprises can use electronic-customs software to declare customs. The process of an electronic-customs declaration includes the following steps:

- Step 1: Log in to the electronic-customs software with the registered account.

- Step 2: Enter information regarding exported or imported goods and related information such as orders, invoices, bills of lading, and documents related to goods.

- Step 3: Calculate and pay electronic-customs taxes and fees.

- Step 4: Print the electronic-customs declaration form and attach necessary documents.

- Step 5: Submit the electronic dossier to the customs agency for processing.

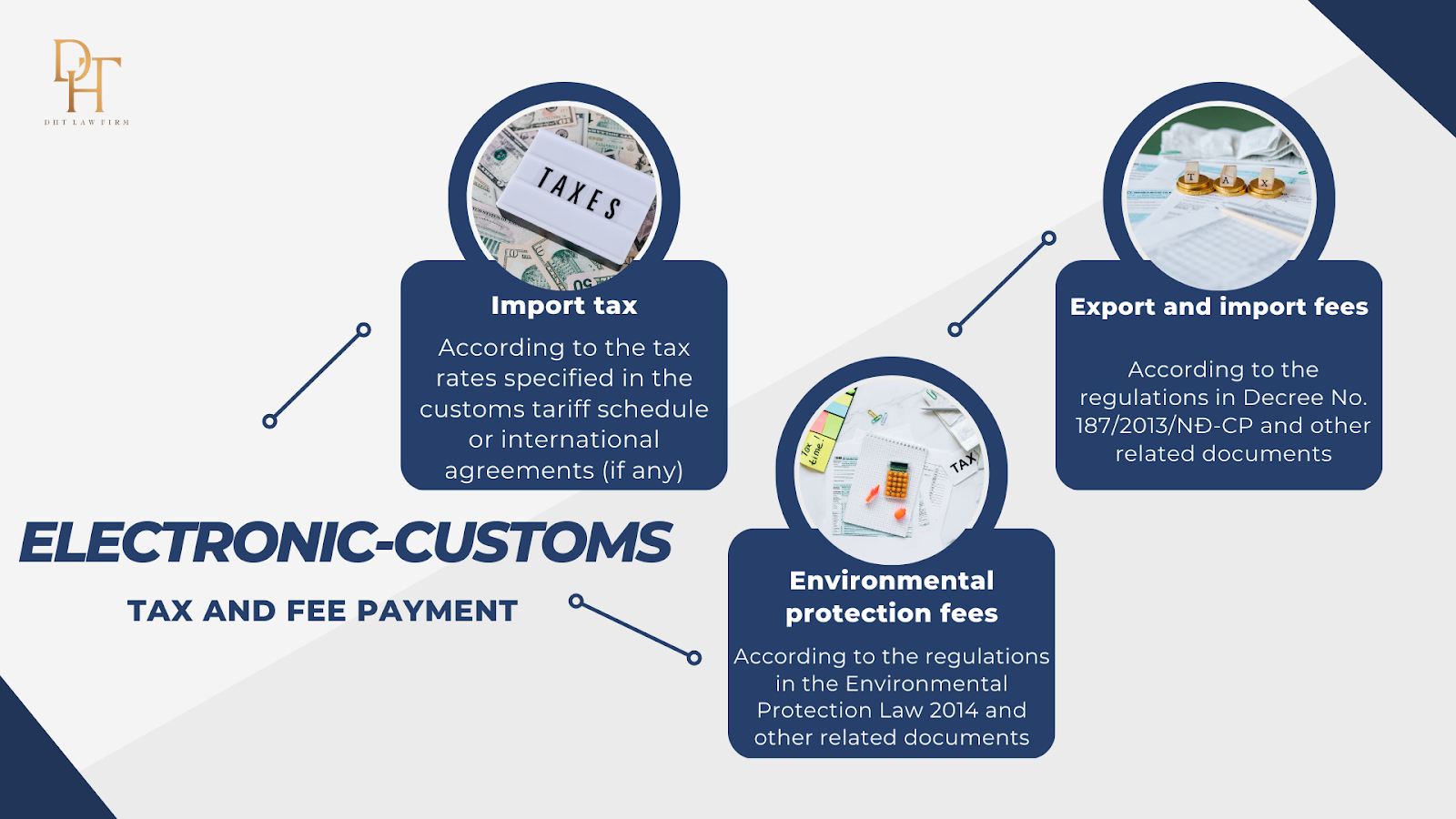

2.2.2. Electronic-customs tax and fee payment.

According to Circular No. 39/2018/TT-BTC, enterprises must pay electronic-customs taxes and fees as below :

- Import tax: According to the tax rates specified in the customs tariff schedule or international agreements (if any).

- Export and import fees: According to the regulations in Decree No. 187/2013/NĐ-CP and other related documents.

- Environmental protection fees: According to the regulations in the Environmental Protection Law 2014 and other related documents.

Enterprises must pay electronic-customs taxes and fees through electronic payment channels licensed by the customs agency.

2.2.3. Electronic-customs inspection and processing.

According to the regulations of Circular No. 39/2018/TT-BTC, customs authorities are authorized to inspect and process electronic-customs as follows:

- Electronic-customs inspection: Customs authorities have the authority to inspect records, data, accounts, images, and other information related to the process of electronic customs procedures. This inspection aims to ensure the accuracy and completeness of the information and data declared on the electronic customs system.

- Electronic-customs processing: Customs authorities are authorized to handle violations related to electronic-customs procedures, including:

- Electronic-customs records are incomplete or inaccurate: Customs authorities may request enterprises or representatives to provide additional information or make corrections to ensure the accuracy and completeness of the records.

- Enterprises do not comply with regulations on electronic-customs procedures: Customs authorities may require enterprises to re-perform traditional customs procedures or take other measures to ensure compliance with customs procedure regulations.

- Enterprises declare incorrectly or violate regulations on exports, imports, or transportation of goods: Customs authorities may apply inspection and processing measures as prescribed by law and other relevant regulations.

The inspection and processing of electronic-customs are carried out in accordance with the regulations of the law and relevant regulations of customs authorities.

2.3. Regulations on export certification or import customs declaration documents

When Exporting processing enterprises want to export goods, they need to register and apply for an export certification at the local customs office. As for importing enterprises, they need to register and apply for an import customs declaration document at the local customs office.

According to the provisions of Circular No. 38/2018/TT-BTC on determining the origin of imported and exported goods, specific cases regarding Vietnam's export certification or import customs declaration documents include:

- With goods that require certification in accordance with the regulations of the exporting and importing countries, an export certificate or import clearance certificate is required.

- With imported goods used to produce exported goods, an export certificate or import customs declaration documents is required.

- With exported goods at a low value (under USD 2,000), no export certificate is required.

- With exported goods to certain special markets, an export certificate or import customs declaration documents is required to meet the requirements of that market.

Certificates of export declaration or import customs declaration documents must be made according to the regulations on content, form, and time limit of Vietnamese law. This ensures the accuracy, completeness, and transparency of information about exported or imported goods. In addition, to enhance the effectiveness of managing the import and export of goods, customs authorities will inspect and process these documents according to Vietnamese law.

3. Conclusion

Above is the entire DHT's advice on the notes related to electronic customs procedures in Vietnam. If you have any questions or concerns in this regard, please contact us for professional legal support and advice.